Problems of Steel

It is difficult not to read bad news about the steel sector in recent months. The future of the ovens in Bizkaia (i.e. AHV) is staggering and the economic situation of the other factories is quite dark. However, fortunately or unfortunately this situation is not exclusive to the Basque Country or the State. Some Scottish kilns were recently closed and in recent weeks the unions have been very concerned about the future of the steel industry in Germany. So what is happening to steel?

Steel is not a new or old product. Although the use of iron (steel is actually a iron alloy) has traditionally been linked to human history, it will be very difficult to find other material that has undergone so many transformations and improvements. As we will see throughout this article, this improvement or evolution is being partly detrimental to steel.

If people are asked on the street what they think about steel, you will get the following answers:

- obsolete industry and urgent closure

- pollution

- sinonimo de paro

- workshops with migrants

- etc.

Unfortunately this opinion is also widespread among some politicians and we always find some technical zarzuela ready to underline that the steel industry is detrimental to the economic future.

However, these negative views do not reflect real reality (for people living in the steel factory environment pollution will not be a joke. However, it is not a technological problem but an economic one. If someone has any doubts, I would invite me to visit Luxembourg and, above all, to visit the ovens called Arbed).

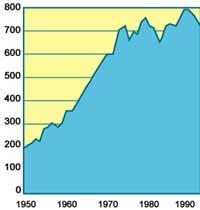

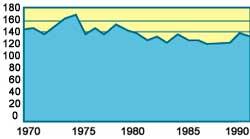

We want to emphasize that this type of industry is not obsolete and that in reality steel will continue to constitute an area of great importance. For this purpose, the attached figure should take into account changes in world steel production in the last 40 years. It is observed that from 1950 to 1970 world steel production experienced remarkable growth. Since the economic crisis of '73, the slope of productive growth has been much lower. In addition, the effects of the economic crisis that occurred around the year 82 and that we are suffering since the year 91 are also reflected in this image. Therefore, according to this graph and taking into account the conjunctural sales, in general, the world production of steel does not seem to correspond to an industrial sector of the “last century”. However, once the production curve is seen, the serious situation of the steel sector in Europe is not well understood. Other factors must be taken into account.

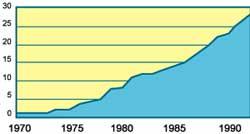

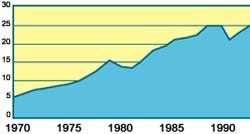

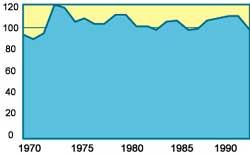

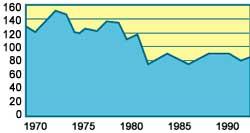

These factors include the productive distribution of steel and the technological level. Regarding the productive distribution of steel, it is advisable to analyze the amount of steel produced in the last twenty years by different states. The following three figures show the production curves corresponding to the USA, Japan and the European Union (EC). In the case of the US, if we look at the picture in general, the behavior of declining production is clearly observed. In the case of Japan, without taking into account cyclical changes, production has remained. Finally, the slope of the CSR curve is negative, with a relatively slow descent.

Regardless of the former communist states, in addition to the US, Japan and the EU, the productions of other peoples must be considered. Brazil and South Korea, which twenty years ago were unknown in the steel sector, now double the production of the Spanish state. As can be seen in the graphs, although the volume of steel produced in 1970 was very small, the amount of steel produced between the two exceeds the third of the European Union.

As a result, the entry of industrializing countries into the steel market has generated strong competition. In addition, the closed Japanese market makes it easy to understand the geographical location of the steel markets: Europe and North America.

The main iron mines in the world are not found in the European Union. Once the last century and throughout this century the most suitable mines, both from the point of view of quality and economy (an example of this we have in Somorrostro), the most minerals come from the outside, being one of the largest suppliers Brazil. After having mineral and being possible to use cheap labor, why not produce steel? That is what the Brazilian authorities thought twenty years ago and the consequences are uncovered. The current price of steel from Brazil, compared to Ensidesa, does not reach half (including the cost of transport). Although the quality of steel in Brazil is not so good, it is difficult to compete with this price.

The situation in South Korea is similar. Being the cheapest labor compared to European standards, the price of steel obtained is also very good. Therefore, the steel produced by Brazil and South Korea is better in price than that produced in our country.

What happens to quality after economic rejection? If the main goal is quality, the problems come from Japan. The quality achieved by Japan in recent years (mechanical properties and steel homogeneity, corrosion behavior, etc.) is the highest in the world.

Consequently, in the face of falling prices and increased competition, the economic situation of the steel sector in the European Union is quite worrying. Since within the Association large companies in the sector depend to a greater or lesser extent on governments, any public investment must be authorized by the authorities of the Association. Therefore, in the debates in Brussels the strength of each state will be very decisive (each defending his own). If one takes into account the steel production of each State as a parameter of force (see figure), we can say without a doubt that the decisions of Germany and Italy, which jointly control almost half of the production, will be of weight.

In this area the future of the Biscay Blast Furnaces will be officially known. Meanwhile, the retirement age of workers has been reduced to 52 years (we will still see that this limit is reduced to 50 years) and with this measure the structure of the workshop (technical teams, etc. ). On the other hand, the disappearance of the horneros at this time is not questioned by anyone (although some newspapers have published other news). Due to social problems, this measure may not be vaporous, but soon comprehensive steel will be hidden from Euskal Herria (from ore to iron alloy). This decision puts an end to the industrial tradition coming from the ironworks and ironworks.

However, it seems that in Sestao an electric furnace factory will be built (to obtain steel the raw material in these workshops is scrap) instead of lubricants. For some the construction of a workshop is fully accepted by the authorities of the Association (for others it is not yet fully linked) and what will be decided in Brussels in the coming months will be the maximum number of productions of this new plant.

With this new plant and taking into account the rest of the electric furnace mills (Acenor, Ucin, Patricio Echeverria, Aristrain, Aforasa, etc. ), despite the loss of furnaces, the Basque Country can maintain steel production. However, we cannot forget that the economic situation of some of the companies mentioned above is not very good and therefore this industrial sector requires basic changes.

In order to cope with external competition, at least different procedures can be applied in theory, although in reality decisions are not so broad. The only objective is to reduce the price of steel. Given that it is not possible to establish the conditions of Brazil and South Korea (since mines and energy are not cheap, the decisions would be to significantly reduce wages or double weekly working hours, or something similar), the only option is technology.

Although decisions are made now, the closure of the blast furnaces in Bizkaia began twenty years ago. Throughout this long term, economic losses have been increasing year after year and decisions and changes were not adequate. If innovations with electric oven plants are not implemented, something similar can happen in the coming years. Therefore, on the one hand it is necessary to renew the technology and on the other to update the knowledge of the technicians.

Technological innovation requires large investments in these plants. To get that money needed, the steel sector should show a much more positive image to society, explaining it as a promising industrial sector. This problem is not just here, and elsewhere decisions have been made to change people's opinions about steel. These campaigns have been based on two points: the use of steel is increasing and the material ecologically suitable.

The beginning of the article highlights that the improvement of steel can be detrimental to it. For some politicians and economists the steel production curve may indicate that the use of this material has reached a limit. Instead, reality is totally inverse. Because steel features are getting better, you need to use less weight to achieve the same goal. This is the case of the car body. Therefore, even though the use of steel is increasing, production in general, measured in tons, shows a different behavior. Thus, returning to the productive curve of Japan, although the amount remains constant in recent years, the use of steel in this country is increasing.

As for recycling, steel is one of the most suitable materials. Once the period of use of steel parts is over, these are the raw material for the generation of scrap steel alloys. Consequently, recycling is almost 100% and, in addition, being a magnetic steel, the selection that must be made in the landfill is very simple compared to other materials. The campaign in Germany to change people's views on steel has been based, for example, on the following approaches.

Finally, as in other areas, it is worth mentioning that in a few years there have been advances in metallurgy. With the use of new tools such as electronic microscopy, different interactions between transformations and variables are now dominated that ten years ago were not well known. These innovations have arisen many times in laboratories (here and in many places in Europe the laboratories of the workshops are of first level) and must be transferred to the workshops. To a certain extent this was not achieved in our workshops, so some high-level technicians are known twenty years ago and control of the variables that appear in some industrial processes is not dominated. Therefore, as the percentage of failures with respect to the leading external factories is higher, the price of the final product is also higher.

In short, the steel industry should not be considered as a technology of the last century, since its use is increasing. However, since competition has increased significantly in recent years, the maintenance of production in Euskal Herria, both by teams and technical managers, requires innovations. Otherwise, despite coming out of the short-term crisis, long-term problems will remain unresolved.

Zu idazle

Zientzia aldizkaria