The euro: the threads of the single currency

The European Monetary System (EMS) was born in the 1970s, after the fall in crisis of the International Monetary System, in order to allow stability among currencies in any way in Europe. The ECU was the account unit of the European Monetary System and its value consisted of all EMS coins. Of course, in the basket of coins each coin had a different weight depending on the economic strength of the corresponding State. The euro in early 1998 is just that, a simple unit of account, that is, a mere reference of account when performing operations. But soon the Euro will also acquire the functions of making and storing internal exchanges, that is, the functions of the common currency, representing traditional national currencies and becoming the single currency of the Member States.

Route so far

Before explaining how this substitution will be and its consequences, let us briefly look at the steps that have been taken so far. In the process of building the European Union the economic base predominates. The commercial point of view is the one that contaminates this process from its origin, which is reflected in its steps. Member States have broken down mutual tariffs and barriers to goods trafficking into a single market.

The Single Market was created in 1992 after a three-decade transition. Since then, in the European common market, goods, services, capital and natural persons, in part, can move freely and are the only tariff and other protective instruments with respect to the rest of the world. In this transition more and more States have joined the European Union. Therefore, for the moment, fifteen states have constituted a single market and the locals carry out the exchanges freely. The only market is the reality that we can already see in the purchase, in the trip or in the banking operations.

The next logical step from a commercial point of view was the entry into force of a single money. Historically, each market, in general, has had its own currency, so the single market has a single currency. In fact, the object of the Pact for the Economic and Monetary Union (EMB) signed in Maastricht was that: the single currency. But the viability of such projects also required an approach to economic realities between different states.

In this way, a three-phase transition was opened to ensure the achievement of MRI. In the first phase, coordination of national economic policy, such as the European Monetary System, should be strengthened. In the second phase, inaugurated in 1994, the European Currency Institute was created, which will be the son of the future European Central Bank, and the Central Banks of the countries became independent of governments. Finally, a single currency will be created in the third phase.

The euro between us

We are in a final phase in which strict monetary criteria are required for states that will amass a single currency (see Figure 1 convergence criteria). This phase has been delayed for two years by the problems arising along the way. Among them is the change known by the EMS, which left out peseta, pound sterling and lira EMS. In addition, the problems of most States in meeting convergence criteria have also influenced the delay of this phase. This allows us a first reflection. Convergence criteria are related to currency and budget, but on the road to meeting convergence criteria costs are not negligible.

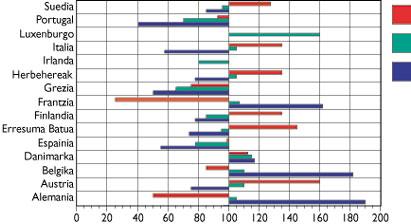

In fact, the activation of anti-inflation mechanisms or the reduction of public spending in the social sphere implies, in addition to an increase in unemployment, a decrease in public protection in favor of it. That is, mandatory convergence in nominal monetary variables opens the way for divergence of real economic variables. Why, then, is convergence required for a single currency, forgetting the divergent influence that currency can have on other real economic variables according to criteria? That is, why approve the unemployment rate or the different per capita incomes between states listed in figure 2, while demanding a rigorous approach to inflation and/or the public deficit?

However, some states fear the consequences this process can have on unemployment, per capita income, etc. This has led to an obsession contrary to the attitude of those who oppose the single currency there and there (the “no” of Denmark, the French strikes...), to delay the same process and initiatives such as the last summit in favor of the “employment” of Luxembourg.

Despite the problems, the third phase will begin this year and in 2002 the euro will definitely replace the other currencies. Meanwhile, from next year the possibility of operating in euros will be expanded: both the monetary and capital markets and the monetary policies of governments will be allocated to euros.

To begin with, this year we will know the names of states that will amass a single currency. Likewise, both the network of central banks of the Member States and the INEM will be part of the European System of Central Banks. Some, like Denmark, the United Kingdom or Sweden, have decided for the moment to be out. Those who meet the criteria of the Maastricht Treaty are known to be included (see Figure 1), but what will happen to those who do not meet any criteria? Will states like Belgium or Italy with a strong public debt be excluded or will the criteria be used flexibly and introduced under the euro from the start?

Once the answer to these questions is known, the next year will definitely establish the unalterable exchange rates between the old currencies and the euro, that is, a permanent relationship between the peseta or the pound and the euro will be established. This step is decisive in the medium term, since it will determine the economic position between the different states: this measure will set the price differences of the goods, services and labor of the different countries and, with it, the price competitiveness with others.

In 1999, the European Central Bank will also take over the EMI and become the axis of the European System of the Central Bank (ESCB). The ESCB will define and implement a single monetary policy and will carry out all its monetary changes and operations in euros.

Next year the public debt of the member states will also be issued in euros, so the financial markets will start using the euro. Therefore, the euro will occupy a prominent place in the international monetary system since next year. In any case, as mentioned above, the currency will not be physically among us until 2002.

What comes with the euro

Transformation is primary. You should not be an expert to realize it. How will we receive the new situation in 2002? The immediate effects that we will know are the headaches that have gone abroad to adapt to the new prices and the lack of burden of exchange when approaching Amsterdam or Dublin. In addition, the prices of goods and services related to the single currency so far with exchange rate variations will be softened. All of them are therefore technical problems related exclusively to exchange. Logically, the immediate benefits of a single currency for the company or the individual citizen that has the European Union as the main scope of action will be more spectacular.

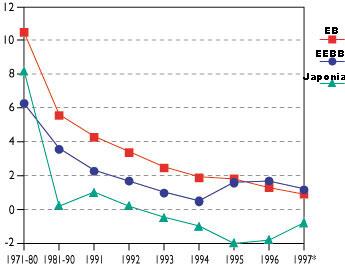

Will the euro influence? Yes, of course, but it is not easy to predict your direction. Most of the agents working in economics will try to make a profit in the new situation. Thus, for example, some sellers of goods and services will try to readjust their prices with a sometimes growing trend to increase their profits. In principle, prices do not have to go up, there may be different price structures in Euskal Herria and in the two territories of Bremen, although they only know one currency (although so far there is only one currency, in Hego Euskal Herria and in Extremadura we have different prices). But in the confusion will be shown some monopolies and the trend we have mentioned from the big companies. However, inflation control is a priority in the RMO Pact and the subsequent Stability Pact, so it does not seem to vary the evolution of inflation in recent years (see figure 3).

Likewise, the trend of banks for their products (loans, deposits, mediation payments, etc.) will be to obtain a greater profit margin by taking advantage of the new situation. Both have the perfect excuse: the costs of adaptation to the euro will increase the costs of the company. Obviously, these special expenses will be relatively light within the cost structures of any company and also temporary. In short, price orientation will depend on the strength and interests of different agents in the market, but there is no economic reason for the price level and current structures to be modified, at least in the short and medium term.

An important qualitative economic change is that States will lose a very important instrument of intervention and that possibility of correcting economic inequalities between countries will be definitively lost. And this will reduce the chances of dealing with real economic problems such as unemployment. On the other hand, the speculative pressure that EMS has exerted so far on currencies will be softened, avoiding sudden devaluations and reducing uncertainty about interest rates.

| Inflation | Interest rates | Public deficit | Public debt | |

Germany (2) | 1.6. | 5.9. | 3rd | 60.8 |

Germany (2) | Documentation | 6.2. | 4.3. | 7th. |

Belgium (2) | Services | Security | 3.3.- Information System | 130.6 |

Denmark (3) | Services | 6.7. | 1.4. | 70.2 |

Spain (2) | 2.5.- Documentation | 7.2. | 4.4. | 67.8 |

United Kingdom (3) | Services | 7.7. | 4.6.- Introduction | 56.2 |

Finland (2) | 0.6 | 7.1.- Evolution | 3.3.- Information System | 61.3. |

France (3) | 1.7. | 5.9. | 4.1. | 56.4 |

Greece (0) | Documentation | 9.6. | 7.9. | Laboratory |

Netherlands (3) | 1.6. | 5.8. | 2.6. | 78.7 |

Ireland (3) | 1.9. | 7.3 | 1.6. | 74.4. |

Italy (2) | 2.2.1.- Waste management | 7.9. | 7.5. | 123.4 |

Luxembourg (4) | Documentation | 6.3 | 0.9 | 7.8. |

Portugal (2) | 2.4.- Description | Other | Security | 71.1. |

Sweden (2) | 1.1. | 7.2. | 3rd | 78.1. |

objective | 3 bottom + 1.5 points 2.60% | 3 bottom + 2 points 8.80% | 3% of GDP | 60% of GDP |

Zu idazle

Zientzia aldizkaria